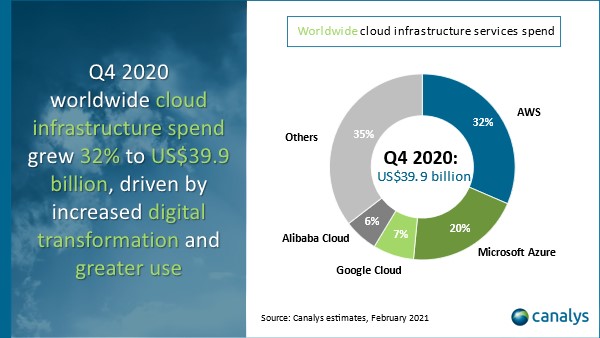

Cloud infrastructure services spending increased 32% to US$39.9 billion in the last quarter of 2020, following heightened customer investment with the major cloud service providers and the technology channel. Total expenditure was over US$3 billion higher than the last quarter and nearly US$10 billion more than Q4 2019 according to Canalys data. This is again the largest quarterly expansion in dollar terms, as continuing pandemic restrictions drove intense demand for cloud to support remote working and learning, ecommerce, content streaming, online gaming and collaboration. At the same time, a gradual recovery in economic confidence stimulated cloud investments by organizations in all industry segments to drive digital transformation. Cloud providers are extending their investments in channel partnerships to maintain high demand rates, and support customers, which will be critical for implementing projects in 2021 and beyond.

For full-year 2020, total cloud infrastructure services spending grew 33% to US$142 billion, up from US$107 billion in 2019. Demand was higher than expected, despite an initial slowdown in large consultative-led projects.

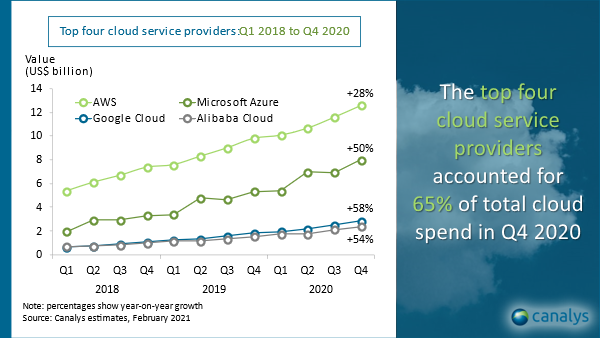

Amazon Web Services (AWS) was the leading cloud service provider again in Q4 2020, accounting for 31% of total spend. After a mixed Q3 in terms of customer performance, AWS had a resurgence in customer investment. This fueled 28% growth year on year for AWS in cloud in Q4 2020. AWS is making investments across its global partner ecosystem to sustain its momentum, including greater support for ISVs, launching new vertical partner competencies, further expansion into distribution to boost SMB adoption, and new partnerships as it extends its hybrid cloud strategy.

Microsoft’s Azure growth rate accelerated once again, up by 50% to boost its market share in the global cloud services market to 20%. Microsoft has focused on driving Azure consumption across all customer segments through annuity sales programs and customer success investments, as well as targeted incentives for its global partner channel. It has also benefited from continued high demand for Teams, Windows Virtual Desktop and other Microsoft services running on Azure as lockdowns tightened.

Google Cloud was the third largest cloud service provider in Q4 2020, with a 7% share. It reported growth of 58% in Q4 2020, as it pushes its ‘open cloud’ strategy emphasizing sovereignty, sustainability and multi-cloud management, and maintains a focus on its six target vertical industries. It has aligned its sales force and channel to these industries as it builds a partner network with industry-specific expertise and deep specializations in its priority solutions, such as machine learning, analytics and data management.

Alibaba Cloud grew 54% in Q4 2020 to account for 6% of the total market. It remained the leading cloud service provider in the Asia Pacific region, including China. It updated its hybrid cloud strategy during the quarter, with the launch of its Hybrid Cloud Partner Program and on-premises appliances targeting small and medium-sized businesses. The program will enable partners to plan, design and resell Alibaba Cloud services with free licenses and unlimited CPU cores.

Demand for cloud services stayed strong across all enterprise customer segments, including industries most affected by the pandemic, such as retail and manufacturing. “The rate of digitalization, led by cloud, is gathering pace. Companies are now more confident about releasing budgets for business transformation,” said Canalys Research Analyst Blake Murray. “Large projects that were postponed earlier in the year are being re-prioritized, led by application modernization, SAP migrations and workplace transformation. Healthcare, financial services and pharmaceuticals are among the industries leading the way, but even those under most pressure are diverting investments to cloud, opening up new revenue streams and diversifying business models.”

At the same time, small and medium-sized businesses continue to turn to cloud services to help them maintain their operations and control costs. The approval of COVID-19 vaccines and the start of mass vaccination programs will further increase business confidence throughout 2021, while remote working and learning will continue. This will maintain dependence on cloud services and drive momentum in spending, though customers will become increasingly aware of the cost, security and complexity challenges of greater cloud adoption.

The technology channel, from global systems integrators and MSPs to resellers and distributors, is playing an increasingly important role in driving cloud growth around the world. All the major cloud providers are increasing their investments in the channel, both to leverage the consulting and managed services capabilities of partners, and to expand sales capacity to drive cloud consumption. Microsoft holds the largest share of the indirect channel with Azure, though AWS and Google Cloud are gaining ground. Meanwhile, as customers deploy different workloads across public, private and edge cloud infrastructures, they are looking for independent partners with capabilities across multiple cloud providers.

“Organizations are turning to trusted business partners to advise, implement, support and manage their cloud journeys, and articulate the real business value of cloud migration,” said Canalys Chief Analyst Alastair Edwards. “Customer digital transformation projects are highly complex, requiring advanced consulting skills, combining deep technical skills with vertical expertise, which the cloud service providers are relying on partners to provide at scale. They are also turning to their partners to drive cloud consumption, and deliver full customer lifecycle support. As organizations start to consider moving more mission-critical workloads to the cloud, they will look to partners to define the right cloud platforms and strategies, as well as solve the most pressing issues around cost management, security, sovereignty and hybrid IT integration.”

Canalys defines cloud infrastructure services as services that provide infrastructure as a service and platform as a service, either on dedicated hosted private infrastructure or shared infrastructure. This excludes software as a service expenditure directly, but includes revenue generated from the infrastructure services being consumed to host and operate them.